Despite the love it gets from Republicans and insurance companies, Medicare Advantage is a lousy program. Multiple news items this week highlight how poorly it operates and how enrollees and taxpayers would benefit from turning it into a Social Security-like cash transfer program.

Medicare Advantage is the part of Medicare where Congress pays private insurance companies to cover enrollees. In general, it is more attractive to healthier enrollees, while traditional Medicare is more attractive to sicker enrollees. More than half of eligible enrollees now choose Medicare Advantage.

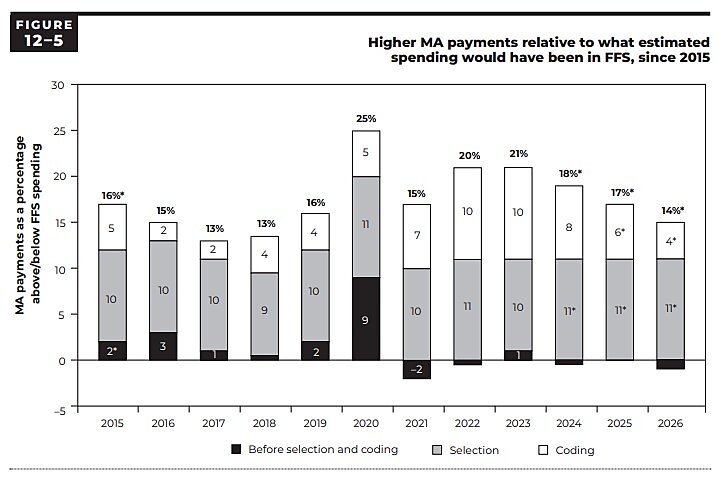

Yesterday, the Medicare Payment Advisory Commission released its March 2026 Report to the Congress. MedPAC concluded, “Medicare will spend 14 percent — a projected $76 billion — more for [Medicare Advantage] enrollees in 2026 than it would spend if those beneficiaries were enrolled in [traditional] Medicare.”

Why? As former administrator Tom Scully infamously quipped, Medicare is “a big, dumb price fixer.” Simply put, Medicare uses a formula to determine the prices it will pay private plans, and that formula sets those prices too high. Those “pricing errors” have persisted for decades. (See figure.)

On Tuesday, Congress’s Joint Economic Committee reminded us that excessive spending in Medicare Advantage indirectly increases premiums for enrollees in traditional Medicare. Thanks to those excessive government-set prices, JEC writes, “in 2025, Part B premiums were, on average, about $212 higher per enrollee.”

The net effect is that subsidies go down for relatively sick traditional Medicare enrollees and go up for relatively healthy Medicare Advantage enrollees. (Since Medicare enrollment is voluntary, an increase in premiums merely reduces the enrollee’s net subsidy.) Once again, government price-setting benefits the healthy over the sick.

Congress could avoid both problems by simply giving Medicare enrollees the cash. Medicare should calculate a per-enrollee payment just like Medicare Advantage does now. But then—as President Trump has endorsed—it should give the money to the enrollee rather than an insurer. That process would automatically calculate and produce larger “Medicare checks” for sicker enrollees than healthy enrollees. Congress could also adjust “Medicare checks” so that lower-income enrollees get bigger checks. Since the government would no longer be setting prices, there would be no more government pricing errors (or insurers gaming the system). Price sensitivity and competition would put downward pressure on prices for medical care, just as they do for things that enrollees now purchase with their Social Security checks.

Finally, today KFF reports that at the end of 2025, insurers terminated the Medicare Advantage plans of 2.6 million enrollees (suggesting the government’s prices were maybe slightly less excessive in 2026 than in 2025). While 98.9 percent of that group could still choose from an average of 25 other Medicare Advantage plans, nearly 30,000 enrollees ended up with no Medicare Advantage plan options. Their only option was traditional Medicare.

“Medicare checks” would also solve this problem. Flexibility in plan design would give enrollees a broader range of plan options than Medicare (Advantage) does. Flexibility in pricing and plan design would allow insurers to offer more durable, long-term health plans, where enrollees and insurers are not subject to the whims and errors of government price-setting. Turning Medicare into a cash-transfer program would help contain spending, improve health care quality, expand choice, and give enrollees more secure, long-term insurance protection.